Need help? Talk to an expert: 8697842776

Form 10E is the mandatory statutory form required to claim tax relief under Section 89(1). Since you are likely finalizing filings for AY 2026-27 (FY 2025-26), it is important to note that even with the transition to the Income Tax Act, 2025, this relief remains a critical mechanism to prevent taxpayers from being pushed into higher tax brackets due to lump-sum receipts of past dues.

Form 10E (Claim Releif of Past Year Income Received Current Year)

Form 10E is the mandatory statutory form required to claim tax relief under Section 89(1). Since you are likely finalizing filings for AY 2026-27 (FY 2025-26), it is important to note that even with the transition to the Income Tax Act, 2025, this relief remains a critical mechanism to prevent taxpayers from being pushed into higher tax brackets due to lump-sum receipts of past dues.

Form 10E is used to "spread" the tax liability of arrears or advance payments back to the years in which they were actually earned. This is applicable for:

Salary Arrears: Belated payments or back-dated increments.

Advance Salary: Salary received for a future period.

Arrears of Family Pension: Received by legal heirs.

Gratuity & Commuted Pension: Subject to specific service year requirements.

Compensation on Termination: Payments received upon leaving a job.

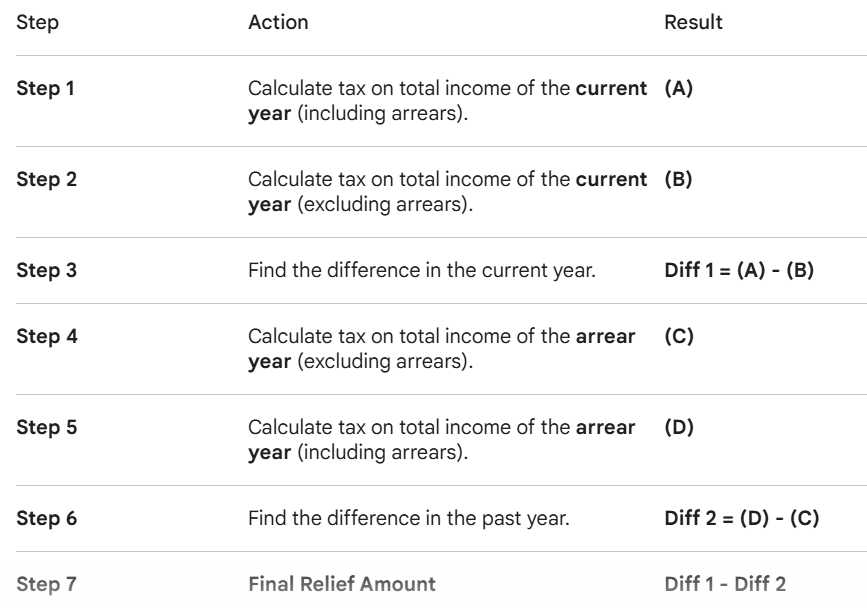

To calculate the relief amount, you essentially compare the tax "hit" in the current year versus what it would have been in the past.

Crucial Rule: If Diff 2 is higher than Diff 1, no relief is available. Relief is only granted if the receipt of arrears actually increases the tax burden.

Mandatory Filing: You must file Form 10E online before filing the Income Tax Return (ITR).

Notice Risk: If a taxpayer claims relief under Section 89(1) in their ITR but fails to submit Form 10E, the Income Tax Department will issue an intimation under Section 143(1) disallowing the relief and raising a tax demand.

Regime Neutrality: Relief u/s 89(1) can be claimed under both the Old Tax Regime and the New Tax Regime.

When filling out the form on the e-filing portal, you must select the appropriate annexure:

Annexure I: For Arrears of Salary or Family Pension.

Annexure II/IIA: For Gratuity (based on years of service).

Annexure III: For Compensation on Termination.

Annexure IV: For Commuted Pension.

Since we are currently in March 2026, remember that income earned during FY 2025-26 is still governed by the Income-tax Act, 1961 and will be assessed in AY 2026-27. From April 1, 2026, the "Tax Year" concept of the 2025 Act begins, but for these arrears, the existing Section 89(1) procedures remain your primary framework.

CONTACT - 8011358502 || 8697842776

CONTACT PERSON - SURAJ KUMAR SARKAR

MAIL US - suraj.sarkar@rongmeifinancialservice.com

Elevate Your Financial Future

(Comprehensive Solutions for Individual & Business Growth)

TAX NEWS & UPDATES

taxupdates.rongmeifinancialservice.com

PROFESSIONAL ADVISORY

advisory.rongmeifinancialservice.com

EXPERT CONSULTATION